Value weighted sample selection is used in auditing when the population consists of monetary amounts (e.g. account balances in the financial statements). The sampling unit is each individual dollar in the account balance. The amounts in the account balance that contain the selected dollar units are picked as the samples. Amounts with a higher value have a greater chance or probability of being selected.

This approach may be used in conjunction with the systematic method of sample selection (i.e. every nth dollar in the population is selected based on a sampling interval) and is most efficient when selecting items using random selection (ISA 530, Appendix 1).

Monetary Unit Sampling (MUS) is a type of value weighted selection.

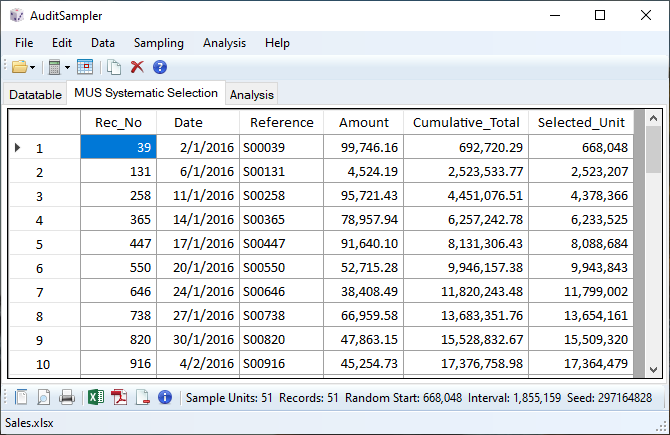

MUS Systematic Selection

When using systematic selection, if the population value is $94,613,131 and the required sample size is 51, the sampling interval would be $1,855,159 (i.e. 94,613,131/51). Each amount in the population is added to a cumulative total. The amount which causes the cumulative total to equal or exceed the random start selected dollar unit ($668,048) is selected as the first sample. Subsequently, each amount which causes the cumulative total to equal or exceed each increment of the sampling interval (i.e. selected dollar units $2,523,207; $4,378,366 etc) are picked as the samples.

- Any amount greater than the sampling interval is selected at least once and very large amounts may be selected more than once (as the amount contains more than one sample unit). Therefore, the actual number of items selected may be less than the monetary unit sample size because the same item is selected more than once.

- Zero and Negative value amounts are not added to the cumulative total and would not be selected. The auditor may choose to review these items separately.

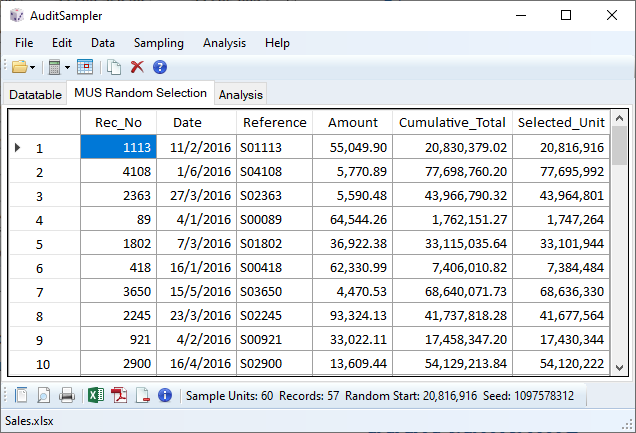

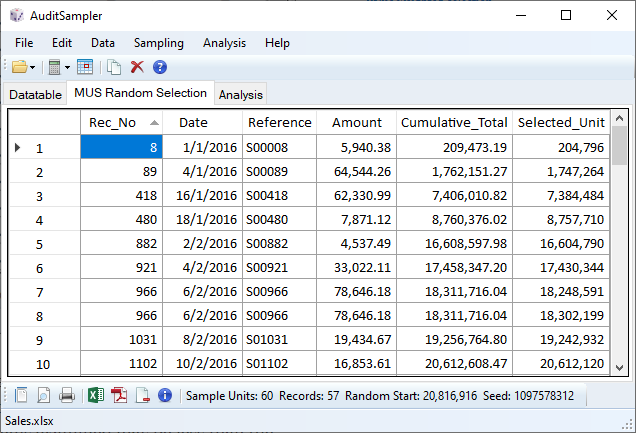

MUS Random Selection

When using random selection, the amounts in the population that cause the cumulative total to equal or exceed the random selected dollar units ($20,816,916; $77,695,992; $43,964,801 etc) are picked as the samples.

Rec_No (Sorted Ascending):

- The same record may be selected more than once if it contains two or more random selected dollar units (e.g. RecNo 966 is selected twice as $78,646.18 contains two sample units). Therefore, the actual number of items examined may be less than the monetary unit sample size because the same item is selected more than once.

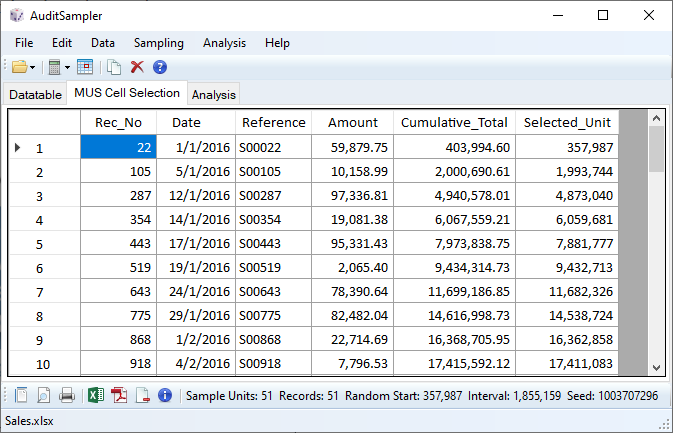

MUS Cell Selection

When using cell selection, the population is divided into equal size cells based on a cell interval (population/sample size). The amount in each cell that causes the cumulative total to equal or exceed the random selected dollar units ($357,987; $1,993,744; $4,873,040 etc) are picked as the samples.

* Screenshots using AuditSampler software.

References

- Arthur J. Wilburn (1984), Practical Statistical Sampling for Auditors, New York: Marcel Dekker, Inc.

- A. van Heerden (1961), Steekproeven als Middel van Accountantscontrole [Statistical sampling as a means of auditing], Amsterdam: Maandblad Voor Accountancy en Bedrijfseconomie 35(12): 453-475. https://doi.org/10.5117/mab.35.13358